"There are known knowns; there are things that we know

There are known unknowns; that is to say there are things that we now know we don't know"

But there are also unknown unknowns - there are things we do not know we don't know"

-Donald Rumsfeld, U.S. Secretary of Defense, 2002

The economic and market environment remains as uncertain as ever as we move into 2013. One does not have to look far to find extreme risks that could propel us sharply in either direction at any given moment in time. Given these vast complexities, examining investment markets as a whole can lead to many conflicting signals. Thus, it is worthwhile to break the market down into isolated component parts to determine what is known as fact and what must be predicted. And by working to simplify the markets, it should ultimately lead to a greater understanding of what we can expect from investment markets in the coming year.

The Known Knowns

The following forces are known as fact for investment markets in the coming year. And none is more significant than the first.

Extremely Aggressive Monetary Policy - One fact we know heading into the New Year is that the U.S. Federal Reserve is ready to print money with wild, perhaps reckless, abandon. Overall, the Fed will inject more than $1 trillion into financial markets in 2013 as part of its QE3 program at a rate of $85 billion per month. And the Fed money printing is likely to be joined along the way by major programs from the European Central Bank, the People's Bank of China and other major global central banks. In recent years, such aggressive monetary stimulus programs have driven investment markets higher regardless of economic fundamentals or persistent threats of crisis. And given the scale of monetary stimulus in the coming year, it is likely that we may see more of the same in 2013. While some have questioned the efficacy of QE3 in this regard since its launch in September 2012, it is important to note that relatively little liquidity has been injected into the financial system to date under this program. This is set to change in a big way starting in January 2013, however, as U.S. Treasury purchases are added just as mortgage backed securities purchases under the existing program begin to pick up speed. In terms of investment impact, this should benefit stocks, high yield bonds and precious metals including gold and silver most. These gains are likely to come at the expense of U.S. Treasuries, particularly Long-Term U.S. Treasuries, as capital flows out of the safety of U.S. government bonds and into risk assets.

Taxes Are Going Up - Regardless of what direction fiscal policy makers chose in Washington DC over the coming year, one thing we know for certain is that taxes are going up. While the impact of these higher taxes may impact certain income earners more than others, everyone in the U.S. will be paying more in taxes than they have in previous years, even if it's 2% more out of their paycheck once the payroll tax cut expires. And if consumers and businesses are sending more of their money to the government to pay taxes, they have less money left over to spend on consumer and capital goods. This is likely to place a drag on economic growth in the coming year, which should presumably weigh on stocks and high yield bonds in favor of precious metals and U.S. Treasuries. But the heavy flow of liquidity from the Fed may help investors to ignore such fundamental truths for yet another year.

Fiscal Policy Paralysis - A fact that is repeatedly reinforced by the Federal government in Washington is that absolutely nothing of substance is going to be accomplished in addressing the critical issues facing the U.S. economy until politicians are up to their knees in the fire of the problem. And even then they are likely to find a way to dither. The recent fiscal cliff debacle highlights this point, as the media has been captivated by a debate over policy solutions that do not even begin to scratch the surface of the underlying problem. For example, the Federal debt has increased by $6 trillion over the last five years, yet we have been tortured for over nearly two months on a debate that struggles to implement even $100 billion in spending cuts. In short, nothing is going to come out of Washington to try and tackle the problems facing the U.S. economy in 2013. Instead, solutions will finally come under consideration down the road when it's potentially too late.

The European Crisis Remains Unresolved - The seeds of the European crisis were sown years ago and began manifesting themselves during the outbreak of the financial crisis back in 2008. And the problem has continued to get worse with each passing year. In 2010 the problem was Greece. By 2011 it had spread to Ireland and Portugal. And in 2012 it had fully infected Spain and Italy. As debt problems continue to mount, economic growth remains insufficient to begin to reverse the trend, particularly as the global economy continues to slow. While coordinated global monetary stimulus may help markets ignore the festering problem across Europe for another year, the problems facing the region and subsequently the world continue to mount. But just like the Fed in the U.S., the ECB appears to stand ready to throw more and more money at the problem. While one cannot solve a debt problem with more debt, the Europeans appear determined to continue trying.

Known Unknowns

The following are forces that are known uncertainties that require careful monitoring and evaluation as the year progresses.

The Global Economy - All signs point to further slowing and the potential for recession in many parts of the world in the coming year. But it remains possible that growth could surprise to the upside, particularly depending on the magnitude of monetary stimulus injected into the global economy in 2013. Any such growth may prove fleeting, but it has the potential to influence investment markets and not necessarily for the better, for it may raise inflation concerns and the thought that monetary policy makers may withdraw stimulus sooner rather than later, which of course they will almost certainly not in the end.

Corporate Profits - Corporate profits have begun slowing with margins already at post WWII highs. And with the global economy set to decelerate in the coming year, many signs suggest that we are likely to begin seeing meaningful profit margin compression as companies have little scope for further cost cuts. Corporations have defied this trend thus far, but it remains to be seen how much longer they can continue to maintain profitability and margins at current levels during the quarterly earnings seasons throughout 2013. Of course, the potential always exists for upside surprise as well, although the odds are becoming increasingly low for such outcomes.

Inflation - When central banks inject as much money as they have over the last several years into the global economy, inflation is an issue that should remain of paramount concern. While policy makers cite that inflation pressures remain largely contained to this point, one could quibble with whether current inflation measures are truly capturing actual pricing pressures. And once inflationary pressures take hold, they can be difficult to contain without a hard press on the monetary brakes. Such a response, of course, has the potential to sharply rattle investment markets.

And the last known unknown is arguably the most important.

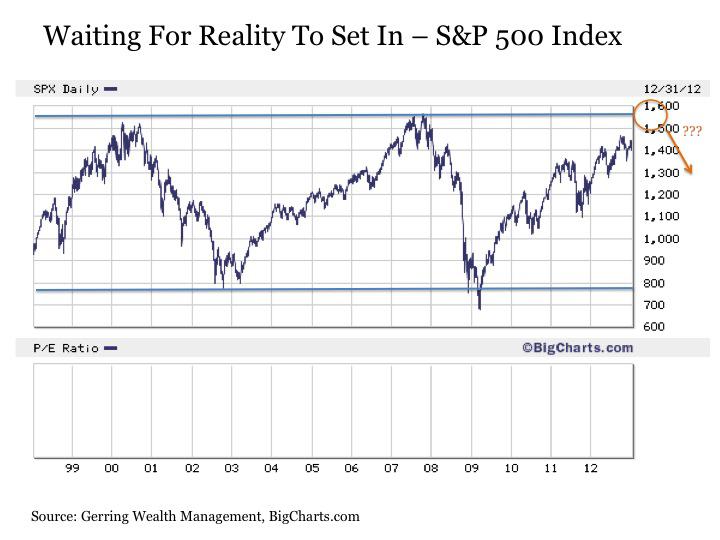

When Reality Finally Sets In - Investment markets have floated higher for years under the influence of monetary stimulus. For the freely flowing money from global central banks including the Fed has enabled investors to completely ignore the fact that little has fundamentally improved since the outbreak of the financial crisis several years ago. In fact, much has gotten worse and precious time and resources have been squandered along the way. At some point, investment markets will finally awaken to the reality of the situation. Exactly when that will occur and what the final catalyst will be remains to be seen, but we will eventually arrive at this inflection point someday. Perhaps this moment will come when stocks arrive at a triple top around 1576 on the S&P 500 Index. But more likely, it will come quietly one day when the market least expects it. Whether this occurs in 2013 or beyond remains to be seen.

(click to enlarge)

Unknown Unknowns

It is the unknown unknowns, or the potential problems that we are not even aware that we should be monitoring, that have the greatest potential to result in a sudden and dramatic shift in investment markets. Potential candidates include the following.

Another Flash Crash - Investment markets have been infested in recent years by high frequency trading programs, which are computer driven models that result in quotes and trades being executed down to the millisecond. We have seen a number of instances in recent years where a breakdown or defect in these models has resulted in highly unusual and disruptive trading activity. While most of these incidents to date have occurred on a small scale, the potential exists for a large-scale market disruption on any given day.

Institutional Meltdown - A good deal of trading activity today occurs in the darker corners of the market, and the potential continues to exist for another Long-Term Capital Management or London Whale type unraveling where a select group of traders or a hedge fund takes on a disproportionately large position that threatens to destabilize a major financial institution or the entire global marketplace. One would have hoped in the aftermath of the financial crisis that measures would have been undertaken to diffuse these risks. But unfortunately, such activities continue to go unabated if not encouraged in the current environment.

Geopolitical Event - Numerous challenges exist across the global political landscape. The situation in the Middle East remains highly unstable with new leadership assuming power in a number of countries across the region. And the recent events in Benghazi have reinforced the idea that the threat of terrorism remains pronounced. Such events have meaningfully disruptive effects on investment markets at any given point in time.

Such is the economic and investment landscape as we enter 2013. It is an environment that is fraught with risk and must be managed carefully. But when considering all of these factors both in isolation and then collectively, we can draw the following conclusions.

Bottom Line

The Fed is set to stimulate aggressively in the coming year by printing over $1 trillion. And other global central banks are likely to join in along the way with major stimulus programs of their own. History has shown that during periods when monetary stimulus is being applied so aggressively and at such a massive scale, risk assets including stocks, high yield bonds and commodities will steadily rise regardless of how fundamentally weak the economy and corporate profits may be. Thus, until this trend is definitively broken, it should be expected to continue.

This notion, of course, raises and important question. What exactly could definitively break the trend of aggressive monetary stimulus supporting higher risk asset prices? The answer is a number of forces may cause reality to finally set in on investment markets, and they all require close monitoring throughout the coming year. These forces include the ongoing crisis in Europe, the potential magnitude of an economic slowdown or corporate profit contraction, the outbreak of inflationary pressures, or some other event that cannot be reasonably anticipated at the present time.

Thus, a hedged investment strategy remains prudent as we enter the New Year. An allocation to risk assets such as stocks, high yield bonds and commodities including copper, oil, agriculture, gold (

GTU) and silver (

PSLV) are all warranted given the degree of money set to be printed in the coming year. A position in TIPS (

TIP) also makes sense along with precious metals and senior loans (

BKLN) to protect against the threat of inflation and rising interest rates. But in recognition that downside forces may eventually overwhelm the investment market euphoria over monetary stimulus or that the stark reality that underlying fundamentals remain woefully insufficient to support stocks and other risk assets at current levels, it also remains worthwhile to complement these exposures with allocations to areas of the market that should perform well under these circumstances. This includes high quality nominal bonds (

AGG), long-term U.S. Treasuries and other longer duration assets such as Build America Bonds (

BAB). Holding allocations in cash or short-term bonds at selected points in time may also be warranted depending on the swiftness or seriousness of a change in market conditions at any point in time.

The coming year promises to provide more interesting times for investment markets and its participants. But a broadly diversified strategy with components that are designed to participate in any further Fed induced upside but can also withstand any unexpectedly sharp and dramatic turns along the way remains a prudent approach in the current environment.

This post is for information purposes only. There are risks involved with investing including loss of principal. Gerring Wealth Management (GWM) makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections made by GWM. There is no guarantee that the goals of the strategies discussed by GWM will be met.

{kind=link}