I had earlier written an article on Intel Corporation's (INTC) share buybacks. I explained that from a strict financial standpoint, that they are a gimmick that add no value. I encouraged smart investors to ignore the gimmick of share buybacks.

One of my colleagues in the Seeking Alpha contributor community has posted a rebuttal to my thesis. You can find the rebuttal in Josh Arnold's article titled Intel's Buybacks Are Not A Gimmick: A Rebuttal.

It is a good article, and investors should read it. I continue to disagree with the conclusions, but I do not have any intention to dispute it, as my position was clear in my original article. Instead, I decided to test if share buybacks add value through tracking the impact of such buybacks on the underlying equities.

For this exercise, I chose the PowerShares Buyback Achievers Portfolio ETF (PKW). This is the description of the ETF from Seeking Alpha.

The PowerShares Buyback Achiever Portfolio (FUND) is based on the Share BuyBack Achievers™ Index (Index). The Fund will normally invest at least 90% of its total assets in common stocks that comprise the Index. The Index is designed to track the performance of companies that meet the requirements to be classified as BuyBack Achievers™. To become eligible for inclusion in the Index, a company must be incorporated in the U.S., trade on a U.S. exchange and must have repurchased at least 5% or more of its outstanding shares for the trailing 12 months. The Fund is rebalanced quarterly and reconstituted annually.

The fund holdings are too many to list, so I have included a link. Sure enough, they include Intel, and in fact 5% of this ETF is made up of Intel. The other big components (~4%+) of this ETF are Home Depot (HD), Disney (DIS), IBM (IBM), Amgen (AMGN), and ConocoPhilips (COP).

So, if share buybacks were to work, we would have expected this ETF to do better than the S&P500, significantly better in fact. The ETF has been around for more than 5 years, so we have quite a bit of market data to test the hypothesis. In particular, interest rates have been low for most of this period, giving more credence to the claim that buybacks made sense in this period. Let's see how that has worked out.

It seems that over nearly 6 years, the cumulative return of this ETF is nearly double that of the S&P500. Very nice, and cause for congratulations? Well, not quite. Here's why.

Note that in the above chart the ETF was virtually identical in total return to the S&P500 till about end 2010. That's about the first 4 years of the ETF's life. Then it started to diverge. So what happened in end 2010? Reported CNN on November 3, 2010.

In its latest move to jump start the sluggish recovery, the Federal Reserve announced it will pump billions into the economy.The central bank will buy $600 billion in long-term Treasuries over the next eight months, the Fed said Wednesday. The Fed also announced it will reinvest an additional $250 billion to $300 billion in Treasuries with the proceeds of its earlier investments.

In other words, QE2 started around end 2010. QE1 went to stabilize the economy, and didn't get a chance to goose the equities of the companies doing stock buybacks. QE2 started the rebuilding process by pumping massive amounts of cash in the economy, and that trend has continued with QE3 and now QE4. That seems to have helped the equities of companies that do share buybacks more than S&P500 as a whole. For the next two years, companies that buy back shares have done better than the S&P500.

To summarize, for the first 4 years of this ETF's life, it tracked the overall market and did no better. For the last two years, after massive amounts of liquidity injection by the Fed, the ETF did marginally better, and for a total of roughly 6 years of its life, on average it returned 1.5% more than the S&P each year.

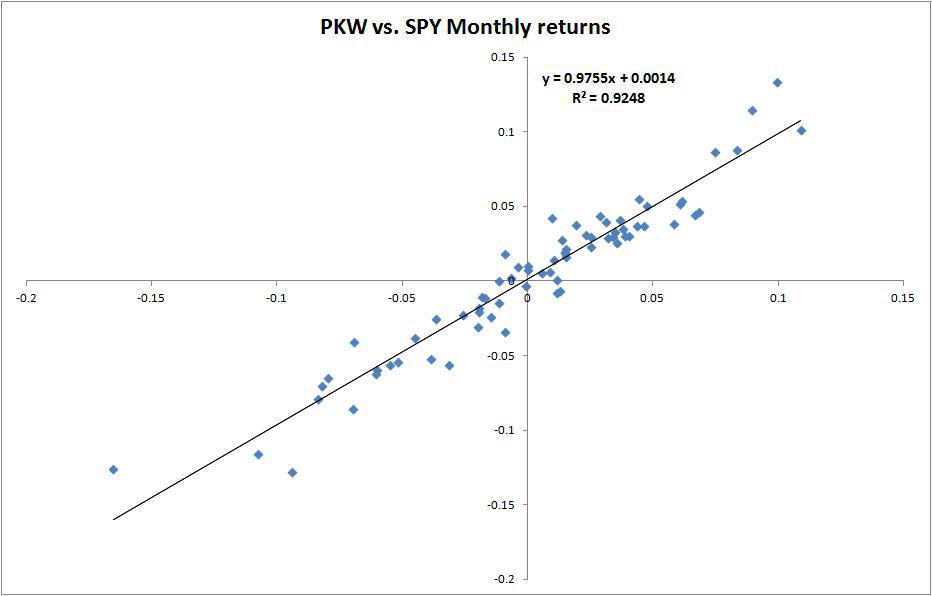

But is this 1.5% statistically significant? I decided to plot the monthly returns of the ETF vs. that of S&P500 (SPY).

(click to enlarge)

The SPY is in the X-axis, PKW is in the Y-Axis. R2 is 92%, which means this ETF basically tracks whatever S&P500 does. The intercept is 0.14%, with 95% confidence intervals of -0.2% to 0.46%. This means that statistically speaking there is no proof whatsoever than the real value of the excess monthly return from this ETF over that of S&P500 is positive. In fact, it could be negative as well.

I think this conclusively proves, at least from a statistical perspective through market testing of 6 years of monthly returns, that share buybacks do not add value. They could do a little better for short periods when massive amounts of liquidity are pumped into the market, but that excess return is in no way statistically significant and could very well be a fluke. So I stand by my earlier recommendation, that smart investors should ignore the gimmick of Intel share buybacks.

Or buybacks from any other company, for that matter. One other note, I just cannot see myself paying excess fees for buying the ETF PKW. Adjusted for excess fees, it has returned virtually nothing over that of S&P500, as one would have expected of course.