In a recent article entitled "Outlook 2013: Americans Are Going Broke," I suggested that negative real wage growth would ultimately constrain the American consumer's ability to support the economy. The thesis was straightforward: wage growth which, on a year-over-year basis is near its lowest levels in recorded history, isn't keeping pace with inflation and as such, consumers will find it more and more difficult to make the discretionary purchases which help fuel the American economy.

In the course of evaluating the various counter-arguments, it occurred to me that there exists a widespread misconception regarding the relative importance of one data point in particular: the household debt service ratio, or, the share of household debt payments to disposable personal income.

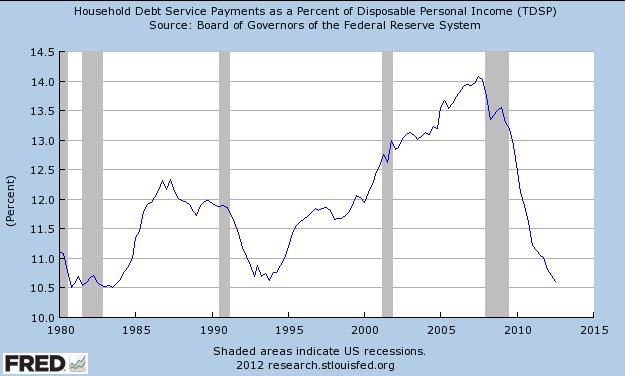

This ratio recently fell to 10.61%, the lowest level since 1983. Here is a visual courtesy of the St. Louis Fed:

(click to enlarge)

The following quote from a recent Reuters article illustrates the typical interpretation of this chart:

A measure of the burden of household debt tumbled in the third quarter to its lowest level in 29 years, which should help free up money for consumer spending and support the economy.

Allow me to say that it is unquestionably true that the less money Americans need to devote to debt service payments, the more they will spend on other items, all things equal. The problem is that in the "New Normal" (a phrase coined by PIMCO's Mohamed El-Erian to describe the post-crisis environment), all things are not equal.

Richer By Default

Before discussing the reason for the outsized decline in the household debt service ratio, it should be reiterated here that households didn't take any proactive steps to achieve the "balance sheet repair" that everyone seems so pleased with. In reality, households deleveraged by default (both figuratively and literally). As I noted in a previous article, it is likely that all of the deleveraging in terms of households is attributable to defaults or write-offs. Here is a quote I have used before from Morgan Stanley's Gerard Minack:

Just as the rise in leverage was built on using debt to buy assets, deleveraging has largely put that process in reverse. Debt reduction can be financed by asset sales or, if that's not feasible, debt write-down. Estimates for mortgage defaults center around $1¼-½ trillion - implying that defaults account for all the net reduction in household debt."

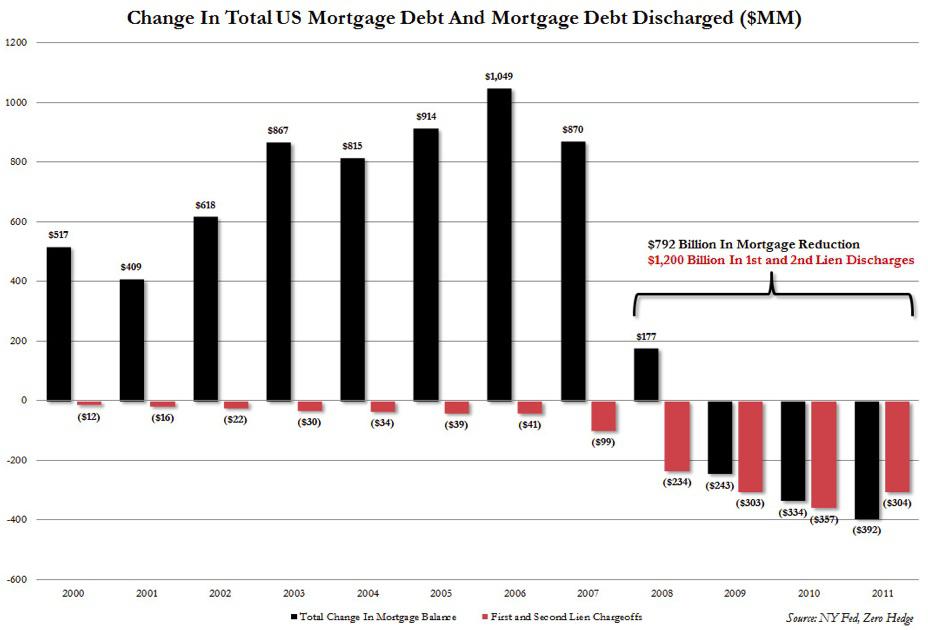

For those who have to see something with their own eyes to believe it, consider the following graph which, utilizing data from the NY Fed, shows the change in mortgage debt alongside the amount of charge-offs for the same periods:

(click to enlarge)

Source: ZeroHedge, NYFed

The often celebrated "healthy deleveraging" appears to have been nothing more than a giant default party. Even those who have written optimistically about the prospects for the American consumer like Bloomberg BusinessWeek's Chris Farrell recognize this sobering reality:

To be sure, about two-thirds of the gain in household balance sheets has come through mortgage foreclosures and credit-card defaults.

More Spending?

Be that as it may, one might still wonder why, given that a lower household debt service ratio necessarily means more unencumbered disposable income, one shouldn't expect consumer spending to rise. In other words, regardless of the reason for the deleveraging, more money should mean more spending.

Not this time. Homeowners or, perhaps more aptly, former homeowners, having just experienced the financial shock of a lifetime aren't likely to simply go right back out and start spending again. As Reuters puts it (article cited above),

While a lightening of household debt burden puts the recovery on firmer ground, it also highlights a hesitance to take on new debt, which could be an obstacle to spending.

For a more academic take on the matter, consider that the Federal Reserve Board's Neil Bhutta recently analyzed the decline in mortgage debt to determine its causes and found evidence in support of both the idea that Americans are hesitant to buy a new home due to the prolonged disruption in the labor market and that reductions in mortgage debt are primarily due to defaults:

First-time homebuying appears to be quite weak [because] credit has been difficult to get. [Additionally] housing demand and the demand for mortgage debt has surely been hampered to some extent by the weak labor market. The growth in outflows can be traced largely to financially distressed borrowers exiting the mortgage market entirely either through sale or default.

If people aren't going to run out and buy a house with their extra money because they are still shell shocked by the crisis, maybe they'll use their new-found surplus of disposable income to simply go shopping instead (let's assume for now that the holiday shopping season numbers didn't just miss expectations by a mile). Not according to the data for U.S. retail sales growth:

(click to enlarge)

Source: YCharts

According to data from the advanced monthly retail trade report which was used to construct the chart above, retail sales growth fell 54.29% on a year-over-year basis in November and is currently running at 3.44% or 25.4% below its long-term average year-over-year growth rate of 4.61%.

Household Debt Service Ratio

Above and beyond the preceding discussion, the real issue with the household debt service ratio is what CreditWritedowns' Edward Harrison calls "the debt service mentality." Harrison notes that:

During the boom and bubble which led up to the financial crisis, many in the financial community looked to debt service costs in the private sector as the only relevant metric to gauge whether debt levels were sustainable.

Harrison describes two theoretical home buyers (Bob and Shirley) who watch as the value of the home they can afford skyrockets as interest rates decline. The problem is that when debt service costs are the only relevant metric, low interest rates paint a false picture of one's financial well-being:

The lower interest rates go, the more affordable any debt load becomes when debt servicing costs are the only constraint. As rates drop toward zero percent, theoretically Bob and Shirley could afford to buy practically any house. But, of course, interest rates don't move in one direction.

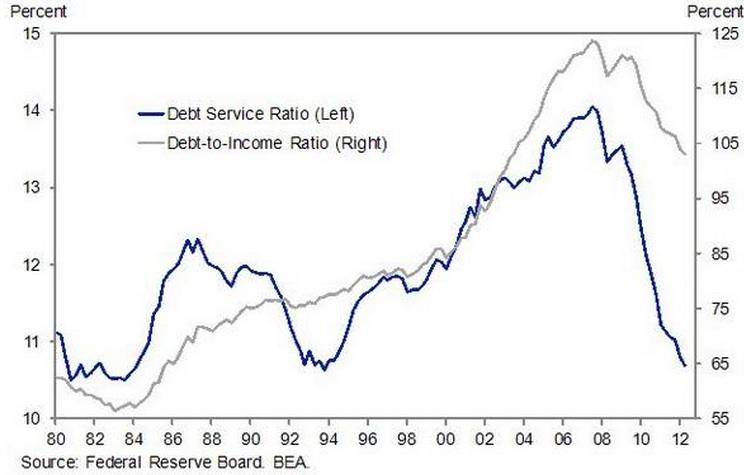

Beware, because this is where the curtain gets pulled back. Have a look at the following chart from Goldman which shows the debt service ratio plotted with the debt-to-income ratio:

(click to enlarge)

Source: Goldman Sachs, Fed

As you can see, it's not the deleveraging that's made the difference. It's the record low interest rates that have made the large debt loads suddenly manageable. Here's Reuters again:

The Fed has sought to help consumers dig out by keeping interest rates near record lows. It has held overnight rates near zero since December 2008 and has bought around $2.4 trillion in bonds to further lower borrowing costs.

As the chart shows, however, Americans' debt-to-income ratio is still above 100% meaning that, according to Reinhart and Rogoff, if American households were countries, they would be in trouble.

The important point is this: if low interest rates were largely responsible for driving down the household debt service ratio (and it appears, given the chart above that this is the case) and rates are currently at zero, it stands to reason that the debt service ratio will go up from here. The only way to escape this conclusion is if Americans deleverage more or start making more money. But neither of these two alternatives seem likely given that 1) there really was no deleveraging in the first place (it was mostly defaults) and 2) wage growth is at historic lows.

What I hope to have demonstrated here is that investors concerned about the outlook for the U.S. economy going into 2013 should be skeptical of overly enthusiastic interpretations of the household debt service ratio. The recent reading for that particular data point is widely heralded as proving that the U.S. consumer now has the financial wherewithal to fuel a consumption-driven recovery. This interpretation is highly misleading.

Investors should remember that the driving forces behind the great deleveraging and the improvement in the household debt service ratio are mortgage defaults and record low interest rates respectively. A country cannot default its way to prosperity anymore than it can print its way to prosperity or become richer by manipulating interest rates. It hasn't worked for the last four years and it won't work in 2013. Expect below average economic growth and similarly disappointing equity returns from (SPY) and (QQQ), as the two will form a negative feedback loop the exact opposite of the wealth effect the Fed so desperately seeks to create.

{kind=link}