Introduction

The majority of investment portfolio returns is due to the mixture of asset classes within the portfolio, with only a minor portion of returns being attributable to the actual individual securities selected within each asset class. This analysis focused on the correlations of several mutual funds with each other, and did not study the investment returns of the overall portfolio mix.

With this in mind, I selected a variety of relatively low-cost, widely available funds belonging to the asset classes:

- US real estate investment trust

- US total equity market index

- Allied Capital (a US Business Development Company, now ARCC, as a proxy for the private equity asset class.)

- US small cap equity index fund

- International total equity market

- US high yield bond fund

- US municipal bond fund

- US long-term treasury bond market

- International developed nation bond market

- International emerging bond market

- Commodity futures index fund.

Methods

The weekly changes of a variety of low-cost mutual funds were analyzed by several statistical analyses. Weekly changes were downloaded fromfinance.yahoo.com, adjusted for dividends and capital gains distributions, from December 2000 to August 2007. This incorporates periods of favorable and unfavorable environments for all of these funds. The results were not normalized for inflation, since weekly inflation data are basically unavailable and probably unlikely to affect investment returns on a weekly basis. However, it is worth noting that over long time periods the effects of inflation are likely to influence the prices and returns of all asset classes.

The investments were chosen due to the availability of long-term returns and their low expense ratios and no-load status. An attempt was made to minimize the number of fund companies. The majority of funds were available at T. Rowe Price and Vanguard. The remaining two assets, ALD and PCRDX, can both be purchased within a brokerage account at either of these two companies. Thus, as few as two mutual funds companies can be used to purchase all of the studied assets.

Mutual funds analyzed: Focus on low expense, no-load

The mutual funds analyzed are summarized below. Not all types of funds are offered by all companies, thus the need for a variety of fund families. Also, there is no business development open-end fund, and thus Allied Capital must be purchased within a stock brokerage account, and these fees are not included in the expense ratio.

Fund name

|

ticker

|

expense ratio

|

company

|

New Era (commodity producer equity fund)

|

(PRNEX)

|

0.66%

|

T Rowe Price

|

Allied Capital

|

5.20%

|

(common stock)*

| |

Small cap index fund

|

(NAESX)

|

0.23%

|

Vanguard

|

Total US equity index

|

(VTSMX)

|

0.19%

|

Vanguard

|

US REIT Index

|

(VGSIX)

|

0.21%

|

Vanguard

|

Total International Equity Index

|

(VGTSX)

|

0.29%

|

Vanguard

|

US high yield bond

|

(VWEAX)

|

0.13%

|

Vanguard

|

US municipal bond

|

(VWALX)

|

0.09%

|

Vanguard

|

US Long-Term Bond Index

|

(VBLTX)

|

0.18%

|

Vanguard

|

International Bond

|

(RPIBX)

|

0.84%

|

T Rowe Price

|

Emerging Market Bond

|

(PREMX)

|

0.98%

|

T Rowe Price

|

Commodity Futures Index

|

(PCRDX)

|

1.24%

|

PIMCO

|

* expense ratio for ALD determined by annual expenses / shareholder equity

| |||

Table 1. Mutual funds and stocks under analysis.

Correlations between equity and bond funds

The first analysis was to assess the relationship between US bond and equity index funds. VBLTX and VTSMX demonstrated a statistically significant, although weak, negative beta of -0.15, and correlation coefficient of 0.06. This supports the validity of incorporating bonds and equities in most portfolio allocations.

Figure 1. Linear regression analysis of broad US equity and bond index funds, VTSMX and VBLTX.

Correlations among equity funds

VTSMX, a Wilshire 5000 broad market equity index fund, was used as the comparator of equity funds investing in commodity producers, small cap index fund, international stock index fund, real estate investment trust index fund, and a business development company. Linear regression revealed varying degrees of positive beta and correlation coefficients. One important finding in this analysis is that the international equities are very closely correlated with US equities. Other equities classes such as commodity producers, REITs, and BDCs offer better portfolio diversification than international equities.

correlation (r2) with VTSMX

|

beta vs. VTSMX

| |

PRNEX

|

0.48

|

0.92

|

ALD

|

0.18

|

0.75

|

NAESX

|

0.83

|

1.11

|

VGSIX

|

0.3

|

0.64

|

VGTSX

|

0.64

|

0.88

|

Table 2. Correlation and beta of various US stocks and mutual funds compared to the broad US equity index fund, VTSMX.

Correlations among bonds funds

VBLTX, a low expense, no-load index fund of long term bonds, was used as the comparator for high yield corporate bonds, high yield municipal bonds, international bonds, and emerging market bonds. None of the alternative bond funds demonstrated meaningful beta or correlations with the long term bond index fund. Thus, bond allocations probably need more granularity in portfolio decisions, with sub-allocations to both US and international bonds, and corporate and municipal bonds as well. All of these other bond sub-types could have risks higher than the typical Treasury fund allocation, but presumably any additional risk will be compensated by higher returns in the marketplace.

correlation (r2) with VBLTX

|

beta vs VBLTX

| |

VWEAX

|

0.01

|

0.06

|

VWALX

|

0.62

|

0.32

|

RPIBX

|

0.27

|

0.48

|

PREMX

|

0.13

|

0.35

|

Table 3. Correlation and beta of various US stocks and mutual funds compared to the broad US long-term bond index fund, VBLTX.

Correlations between international developed and emerging market bond funds

RPIBX and PREMX, representing developed and emerging market international bond funds, respectively, were analyzed. RPIBX had a beta of +0.28 and a correlation coefficient of only 0.08 compared to PREMX, suggesting there is validity in incorporating both funds as alternative bond fund investments. Besides focusing on different types of sovereign debt, another difference between the funds is that the developed market bond fund, RPIBX, is unhedged with respect to foreign currency, while PREMX is currency-hedged. Despite this difference, both funds are non-correlated to US long term bond index fund, as demonstrated earlier. Since the emerging market fund, PREMX, shows lower correlation and beta than RPIBX when compared to VBLTX, PREMX would be a reasonable single international bond fund.

Figure 2. Linear regression analysis of international bond fund (RPIBX) vs emerging market bond fund (PREMX).

Business development companies: a surrogate for private equity / venture capital?

Another surprising finding of this study was the extremely low correlation of the business development company , Allied Capital , with the general US stock market (r2= 0.18). This company is basically a managed portfolio of mezzanine debt of middle-market companies (startup companies that are non-public, competing in the space of private equity and leveraged buyouts, and also venture capital according to some experts). While trading as a single stock, it represents an entire portfolio of over 100 investments in portfolio non-public companies. I hypothesized that this company might appear somewhat correlated with small capitalization equity fund (NAESX) and high yield debt (VWEAX). However, the investment returns of ALD were essentially non-correlated with all studied funds. This is a powerful finding, suggesting that BDC's may represent a tiny, relatively undiscovered independent asset class.

US High Yield Corporate Bonds (VWEAX)

Another surprising finding was that high yield bond funds were relatively uncorrelated with both equity (r2 = 0.08) and bond index funds (r2= 0.01). These data reveal essentially a complete lack of correlation, suggesting that high yield bonds are an effective diversification tool and should be allocated as a separate asset class.

Figure 3. Linear regression of high yield corporate bond market (VWEAX) compared to US total equity index fund (VTSMX) [top chart], and US long-term bond index fund (VBLTX) [bottom chart]

US Real Estate Investment Trusts

These findings agree with common recommendations showing a diversification benefit of real estate investment trusts (REITs) in a portfolio, as represented by VGSIX. The beta of this fund compared to VTSMX (Wilshire 500 broad index fund) was only 0.63, with a correlation coefficient of 0.30. This correlation was lower vs VTSMX than either the small cap index fund or the total international equity index fund.

Commodity Futures Fund, compared to Commodity Producer Equities

PCRDX, the PIMCO Commodity Real Return Fund, was tested against other funds, since commodities are often recommended as a diversification tool. PCRDX was uncorrelated with broad US equity and bond funds (VTSMX and VBLTX).

PCRDX was weakly correlated with the New Era fund (PRNEX), with a correlation coefficient of 0.30. However, the weak degree of this correlation argues against the often-heard argument that commodity producer equities can be used as a surrogate for commodity futures exposure. In fact, commodity producer equities have a stronger correlation with the overall stock market , which had a correlation coefficient of 0.48. In other words, commodity producer equities are affected more by what happens in the broad US equity market than with what happens to commodity markets.

Figure 4. Linear regression analysis of commodity producer equity fund (PRNEX) compared to commodity futures index fund (PCRDX) and US total equity index fund (VTSMX).

Risks

Reliance of historical correlations may prove risky in times of market turmoil, as asset classes tend to show increasing correlations during times of economic crisis. Also, this study did not include the effects of taxes on investment returns. Because some of these investments are considered tax-inefficient, they might be better suited in tax-deferred accounts.

A building block approach toward endowment-style portfolios

The simplest portfolio of relatively uncorrelated assets would consist of VTSMX and VBLTX. However, this analysis has highlighted a number of investments that are non-correlated with both of these investments.

The most simplistic portfolio would be broad US equity and bond funds:

- VTSMX

- VBLTX

Based strictly on correlation coefficient and betas, one suggested order of addition of other asset classes to the simplistic VTSMX/VBLTX portfolio is as follows:

- PCRDX - commodity funds

- PREMX - emerging market bond fund

- ALD - business development company (ARCC now)

- VWEAX - high yield corporate bond fund

- VGSIX - real estate investment trusts

An additional tier of diversification can be considered for investors desiring an even more complicated portfolio:

- RPIBX - international bond fund

- VGTSX - international equity index fund

- VWALX - Municipal bond fund

Incorporating alternative asset classes with target-dated funds

For investors wishing a simplified portfolio offering maximum diversification with a minimum number of funds, the use of a target retirement allocation portfolio, such as the low-fee Vanguard Target 2035 (VTTHX), could be combined with several additional funds as follows.

First, here is the weighting of the Target 2035 fund itself:

Target 2035 fund - asset weighting:

| |

VTSMX

|

71.400%

|

US bond

|

10.500%

|

international equity

|

18.100%

|

In order to achieve further diversification, this Target-dated fund could be combined with other funds from this analysis, in the following weighting:

- VTTHX 60%

- PCRDX 10%

- PREMX 10%

- VGSIX 20%

Conclusions

Endowment-style asset classes are available to individual investors through low cost mutual funds. Rudimentary statistical analysis does appear to support the theory behind the inclusion of less common asset classes, and that this approach may lower the overall beta of a portfolio by including relatively uncorrelated asset classes. Other issues such as portfolio complexity and tax planning may be other considerations for the individual investor before pursuing this approach. The analysis presented here is pre-2007, and a subsequent analysis will illustrate whether or not situations have change in the post-crash environment. Thank you for reading.

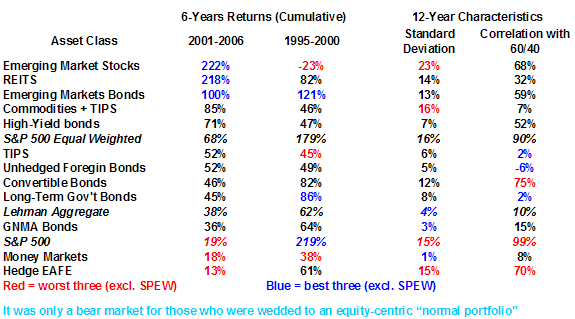

Appendix:John Mauldin's Asset Correlations

(click to enlarge)

Source: accessed online, Millenium Wave Online , September 1, 2007